Why I Passed On A Six-Figure SDE Net Income Business

Why headline SDE isn't always attractive

Hi there! Welcome to another post from our SMB newsletter where we post insightful trends and interesting deals in the SMB space.

If you’re interested in getting these types of emails, hit the subscribe button below. It’s free!

With that said, let’s get into today’s post.

Attention Grabbing Headlines

Have you started your acquisition journey and come across headlines for listings that immediately sound good so you click through to read more?

Yeah, usually, but not always, those are too good to be true. Let me give you an example of just this without giving too much information because I did sign an NDA.

I came across a business with a headline that read

Fitness Franchise with over 6-Figure Net Income!

I’m paraphrasing the title so that you can’t just go ahead and google it but this headline alone covers three main points.

It’s a franchise business so you’re under the assumption that you’ll be getting corporate support for a fee

It’s fitness so could be capital intensive (get an uptick in depreciation in asset purchase) or some type of low capital intensity studio

Six-figure net income sounds great!

There really wasn’t anything that threw off a worrying feeling. The multiple was ~3x SDE which is the average for most fitness businesses being sold and the sales seemed high enough that the margin made sense.

However, the problem is when you start to look under the hood during diligence which changed the whole thing completely. It’s still up for sale by the broker today even though I started talking to them in August of last year if that paints you any picture.

Diligence Discovery

So like most fitness businesses during COVID, there were obviously tough times that needed a lot of effort to generally survive. The owner stated just how much memberships dipped because of state-wide closures and how they had to give discounts in order to get people back quickly.

This didn’t really bother me because that made intuitive sense. In the back of my mind though I was already thinking about how margins were getting hit because of that.

But then again, the business is making over six-figure net income so it had to have bounced back meaningfully.

But just like most people, numbers can’t lie. You can try to finesse the numbers but eventually, everything comes out.

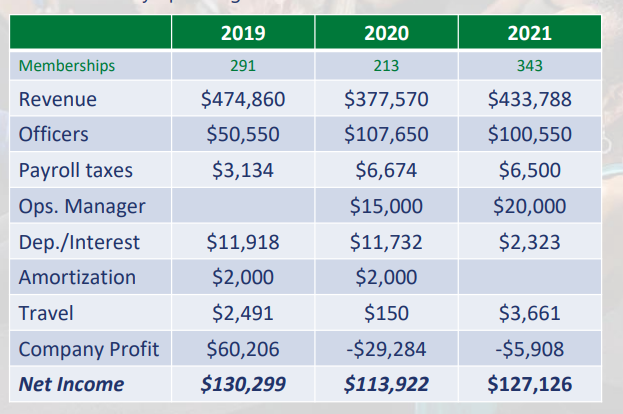

This brings me to the chart in the CIM that basically told me everything I needed to know in about 30 seconds.

I’m going to let you analyze the above chart and see how many things you can determine from it and if you think it makes sense to pursue the opportunity.

After you’ve done that (or not), take a look at all the reasons why I passed on it.

1) Memberships

When I say memberships, I don’t mean the absolute number of memberships, I mean the revenue of the memberships.

In 2019, 291 members equated to ~$475k in sales, or ~$1,632/member for the year.

In 2021, that same equation resulted in ~$1,265/member, or a decrease of ~22%.

Not good but I get it, it’s an uphill battle getting people back.

2) Officer Salary

For those that don’t know, the “officers” line item refers to owners’ compensation. The jump from 2019 to 2020 is understandable because at the run rate, the owner could have afforded to pay herself more.

However, this is BS in my mind because we went into lockdown in March and many states didn’t come back online until summer or even after that for fitness centers.

That >100% increase wasn’t warranted and thus really put the company in the red. Even in 2021, the owner only dialed it back a few thousand after losing ~$29,000 at the company level.

I understand there are tax implications of that but still, you’d rather not see that especially if you’re trying to convince a bank to give you a few hundred thousand dollars to buy the company.

They want to back less risky, financially stable businesses whose owner isn’t milking it for self-gain to prop up numbers.

3) Company Profit/Net Income

It’s pretty obvious but the company isn’t making money, the owner is. The owner makes out with over $100,000 a year but at the expense of the company.

While this technically isn’t “wrong”, it’s not optimal since the obvious goal is to make as much as you can to pay yourself a nice salary while tucking away money for the business as well.

Also, the net income is indicative of add-backs that we don’t necessarily see based on this preliminary chart. While we do see the salary, there’s another ~$27,000 not fully accounted for.

I could tell it partially comes from travel and interest/depreciation but where is the rest? Probably something that would have to be an expense anyways.

Un-Underwritable

Yeah, I just made up that word but it sounds good for this example. If a company doesn’t make enough money to make a bank feel that the investment has enough margin of error for an acquisition to be sound, it won’t fund it.

Let’s see why in my napkin math.

So taking the table above and applying my own rationale, I could ascertain that a lot of the expenses in order to bridge the gap between what was given and the company profit came from traditional things like; employee salaries, misc stuff like accounting, etc., and a simple franchise fee.

The wages come from paying six workers an average wage of $17.50, for 40 hours a week, for 52 weeks a year. Yes, I understand that can vary widely but the point of this simple math is to pressure test it with simple parameters.

For 2022, the owner let me know that they’re on track to do ~12% y/y sales growth. I factored in zero growth for owner wages and depreciation/interest.

Amortization I wrote off to be conservative.

I calculated a new franchise cost based on the fee that they told me and then held margins steady for the other items. Again, to be conservative.

Presto! We have company profit, but not much.

While now the company is making more money, here comes the problem with funding.

Now the benefits of the SBA are that you can get some serious benefits when it comes to the term length on the loan. Typically, it’s 10 years which means that a fully amortized loan can be good since you can lower your monthly payments since the duration is better than traditional 3-year notes.

For the equity, you can put as little as 5% down for some deals but since this company is in the best financial health, I marked it at 20% which will help cover all the misc fees.

But, the problem is the debt rate. SBA loans run off of the WSJP rate plus a spread. Typically this spread is 2 - 300 bps.

If you factor in a terminal rate of 11%, this debt gets expensive but not out of the ordinary for deals nowadays.

However, with the benefit of a 10-year amort, the 11% on 80% LTV makes the annual payment ~$68,000.

That immediately wipes away any gains that you could expect from the business. So while in the second table, I modeled improved company profitability, the summation of my model (~$130,000 in “cash”) gets cut in half with the debt that you’d take out to fund the deal.

No bank and I mean no bank will underwrite that. Hence, why the business still hasn’t sold.

Bottom line

While headlines might be good for attention grabbers, once you peel back the onion, you really find out what stinks.

Always remember to pressure test the math!

If you enjoyed today’s post, please hit the subscribe button below.

Until next time,

Paul Cerro | Cedar Grove Capital

Personal Twitter: @paulcerro

Fund Twitter: @cedargrovecm

HoldCo Twitter: @cedargrovech